“East European Council” starts publication of materials of closed modelling-game which took place on the 10-11th of December in Warsaw under the support of NATO and in cooperation with the “New Eastern Europe”.

The first positioning document – analytical research of economic situation in the Russian Federation.

It is a basic document. It can be used during modeling game. If you have some additions or remarks, we will be grateful.

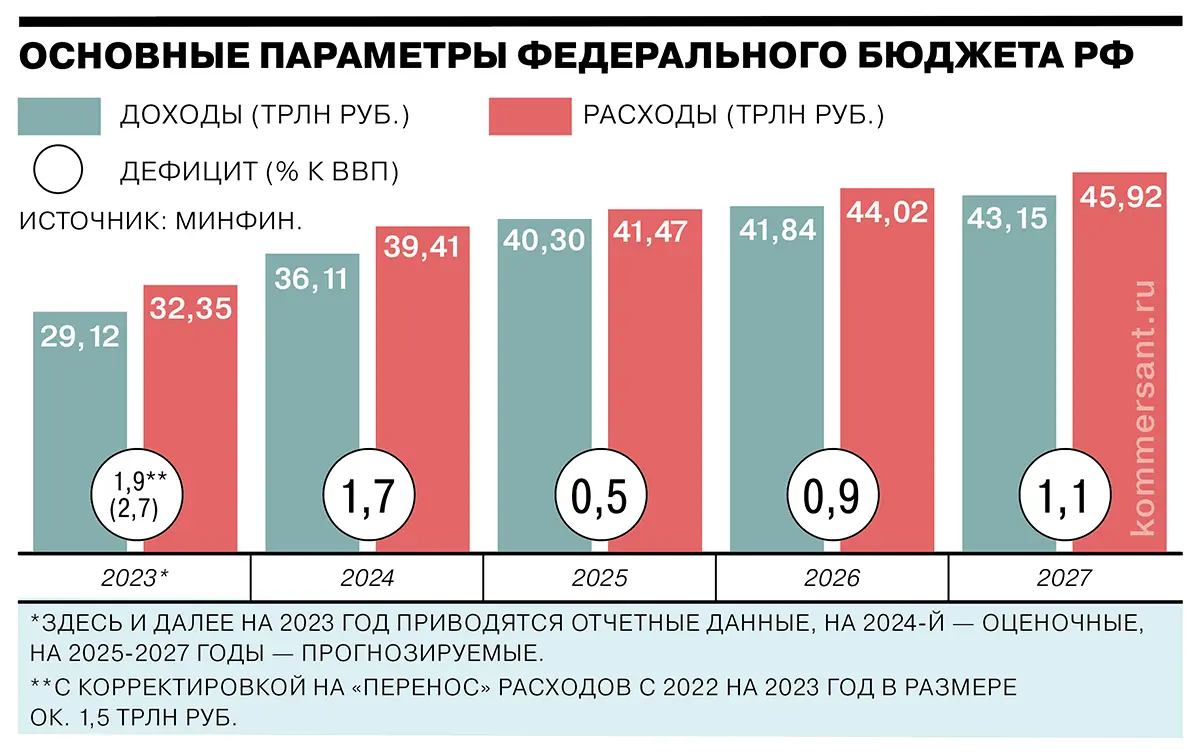

The Russian Federation plans to increase budget spending on defense and the military-industrial sector in the draft budget for 2025 to a record 13.5 trillion rubles ($140 billion). The high level of military spending will remain during 2026 – 12.8 trillion rubles – and 2027 – 13.1 trillion rubles. These circumstances testify to the readiness of the Russian leadership for further militarization of the economy and preparation for the continuation of the war.

Implementation of the 2024 budget and plans for the 2025 budget

After the record spending on defense is carried out in the current year – 10.4 trillion rubles, the peak of spending on the defense sector is expected in the next one.

For a better understanding of the correspondence of the political intentions of the Russian leadership to the real assessment of financial resources, a comparative table of key indicators has been created:

|

2024 |

2025 |

||

|

Expenditures |

Income |

Expenditures |

Income |

|

39,41 trillion rubles |

36,11 trillion rubles |

41,47 trillion rubles |

40,30 trillion rubles |

|

Deficit |

3,3 trillion rubles |

Deficit |

1,17 trillion rubles |

|

Expenditures on national defense |

Expenditures on national defense |

||

|

10,4 trillion rubles – 6% GDP |

13,5 trillion rubles (135 billion dollars) – 6,2% GDP (32,4% of budget expenditures) |

||

|

Income from oil and gas sector (expecting) |

Income from oil and gas sector (expecting) |

||

|

10,98 trillion rubles (29,53% from all income) |

9,27 trillion rubles (23% from all income) |

||

The evaluation of both budgets confirms 4 fundamental problems of the Russian economy, the solution of which is impossible while maintaining the existing defense expenditures.

1) Systemic budget deficit. At first glance, the problem seems under control, since the deficit in 2023 was only 2% of GDP (when compared with some EU countries – for example, France, where the indicated indicator reaches 6% – Russian statistics seem far from problems).

However, an important fact is that traditional indicators of economic stability do not fully allow us to assess the real situation in Russia.

The most objective conclusions can be obtained only in case of analysis of the actual turnover of funds – recording of income and expenses.

Since the beginning of the full-scale invasion, the budget deficit has increased significantly – for the period from 2022 to 2024, Russia will lose a total of approximately 9.82 trillion rubles, which had to be compensated with internal reserves.

For comparison: in 2019 a surplus of 2 trillion rubles was obtained, in 2020 there was a deficit of 4.1 trillion rubles due to the pandemic, but in 2021 the economy began to successfully recover and the surplus amounted to 0.5 trillion rubles.

Thus, during the war in Ukraine, the total deficit of the Russian budget exceeded the indicators of the crisis caused by the pandemic by 58%.

It is necessary to pay attention to the fact that from 2025 to 2027 the budget will maintain a permanent deficit. If it looks quite positive in terms of GDP (2025 – 0.5% of GDP; 2026 – 0.9% of GDP, 2027 – 1.1% of GDP), in real monetary terms the situation will look much more complicated (2025 – 1.17 trillion rubles; 2026 – 2.18 trillion rubles; 2027 – 2.77 trillion rubles).

This means that over the next 3 years in total, Russia will need to replace the deficit in the amount of 6.12 trillion rubles.

At the same time, the forecasts for 2025 already look too optimistic and there is a high probability that the budget will have to be revised in the middle of the year (as it already happened this year, when the Ministry of Finance overestimated expectations from oil and gas revenues by approximately 0.5 trillion rubles).

Covering the deficit will require further use of domestic reserves, which is reflected in the second and third problems.

1) Reduction of the National Development Fund (NDF).

Russia managed to “close the hole” of the budget deficit in 2022-2023 with the funds of the National Development Fund. The Ministry of Finance is counting on a similar maneuver in 2024 and in subsequent deficit years. One of the main factors of ensuring stability is a systemically created “financial cushion”. However, statistics show a threatening trend for the Russian economy.

First of all, Russia is unable to dispose of all gold and foreign currency reserves, as approximately 300 billion dollars are “frozen” in international accounts.

Secondly, despite the fact that the total volume of the NDF is approximately 12 trillion rubles (as of the beginning of 2024), its structure includes both liquid assets (money that the Ministry of Finance can freely dispose of) and illiquid assets (long-term bonds, investments in infrastructure projects, etc.). In the latter case, these are the funds that are on the balance sheet, but cannot be promptly directed to replace the surplus.

The amount of liquid assets reaches 5 trillion rubles (approximately 55 billion dollars).

A simple comparison of the expected deficit with the NDF creates conditions for a scenario in which the liquid part will make it possible to compensate for the deficit of 2024 and 2025, but in 2026 the Ministry risks completely exhausting the fund, which will put the Government in an extremely difficult situation.

At the same time, there are no guarantees that the deficit in 2025 will not go beyond the optimistic plans of the Ministry of Finance, which will bring the scenario of the exhaustion of the NDF closer.

Replenishment of the NDF has rather dubious prospects. In the long term, long-term investments, bonds, etc. can be partially transformed into liquid assets. However, this is a long process.

The rule of transferring the surplus from oil export revenues (if the price is more than 60 dollars per barrel, the difference is sent to the NDF) does not seem to be effective in the conditions of a deficit budget.

Russia has a rather limited toolkit for correcting the threatening trend.

The first option is currency devaluation, but in conditions of high inflation and Central Bank rates, this method is quite dangerous. That is why the future budget does not foresee a significant devaluation – the average exchange rate is set at the level of 96.5 rubles per dollar.

The second option is external borrowing, which appears to be a critically difficult task in the current circumstances and forms the third structural problem.

2) Low prospects for opening credit lines abroad or attracting foreign investments.

In the conditions of war and sanctions, it is critically difficult for the Russian economy to attract foreign investments. According to the results of 2023, their inflow amounted to slightly more than 8 billion dollars, which is an insignificant indicator.

Prospects for opening external credit lines are not yet visible. The Russian side is actively working on establishing cooperation in the banking sector with the PRC, but Chinese partners are not taking any risks to avoid being subject to sanctions.

Various international platforms, such as the BRICS summit, so far achieve certain political goals, but do not provide Russia with concrete results in the financial sphere.

Without external investments and loans, Russia will have to rely only on its own resources and export revenues.

3) Maintaining dependence on the export of energy carriers.

Despite the frequent optimistic assessments of the Russian leadership regarding the reduction of dependence on energy carriers, they will continue to play a key role in Russian exports. If it were not for the realization of oil and gas, the Ministry of Finance would have had to raise taxes even more due to the lack of possibility of real export diversification.

Russian exports in 2023 reached the mark of 425 billion dollars and 60% of its structure consists of mineral fertilizers – primarily oil and gas.

The dependence on the oil and gas sector on the Russian budget is especially indicative. If in 2024 the budget revenues will amount to 36.11 trillion rubles in total, then almost 1/3 of them (30.41%) are tax deductions from the sale of oil, oil products and gas. In total, they will fill the budget by 10.98 trillion dollars (which is approximately 114 billion dollars).

Oil

Sanctions reduced the profitability of the Russian oil complex, but did not stop it. Russian exporters have adapted and successfully sell their products even in the face of economic restrictions. The creation of a powerful shadow fleet, which already has 307 ships and is systematically growing, helps in this, as well as the possibility of registering and insuring ships in the jurisdictions of different countries.

Effective countermeasures of the Russian side led to the fact that Russian companies managed to reorient the majority of raw materials from European markets to alternative destinations – mainly China and India. If the total export of oil amounted to 240 million tons, then 189 million tons fell on the indicated two countries.

Thus, more than 79% of oil for the results of 2023 was exported to them, another 7% to other countries from among the representatives of the so-called south, which Russia calls “friendly”, and approximately 14% to countries that Russia identifies as “unfriendly » (including in the EU).

Chinese direction

Chinese importers received approximately 107 million tons of oil from Russia in 2023, which is almost 45%. Russian companies have become a major player in the Chinese market and have earned more than $60 billion in revenue.

Indian direction

Indian importers received approximately 82 million tons of oil from Russia in 2023, which is approximately 34%. Thanks to exports to India, Russian companies received 37 billion dollars in revenue. Statistics indicate that the average price of Russian oil for India during the year was 61 dollars, which is slightly higher than the “price cap”.

It is worth noting that in 2023, India has established itself as an influential exporter of oil products to the EU markets. Indian products were actively imported to the Netherlands and France. At the same time, such growth of the Indian oil refining complex directly depends on cheap Russian oil, which encourages Indian producers to increase purchases.

Additional routes

Turkey began to play an important role in the organization of Russian oil supply chains. In 2023, Russia exported an estimated 10.7 million tons of oil to Turkish refineries (and a similar amount of petroleum products). It is important that thanks to its own oil refining infrastructure and favorable logistics, Turkey has become a de facto transit hub where Russian oil arrives and after processing is exported to EU markets.

Transit through the southern branch of the Druzhba oil pipeline to Hungary, the Czech Republic and Slovakia is maintained. In 2023, it was at the level of 13 million tons, which allowed the Russian side to receive approximately $5.7 billion in revenue.

Gas

Despite the loss of a significant part of the EU gas market and Gazprom’s significant financial losses, gas continues to be an important component of Russia’s export market. It is routed to both European and Asian markets via pipeline infrastructure and by sea. Novatek plays a key role in the establishment of LNG gas supply channels.

LNG gas

According to the results of 2023, Russian exporters sold approximately 45.4 billion dollars worth of LNG natural gas. The key areas are Asia (approximately $32.7 billion) and Europe ($12.7 billion). Despite the policy of abandoning Russian energy carriers, EU countries continue to actively receive Russian liquefied gas. It partially replaces the gas lost after the explosion at the Nord Streams. At the same time, the main consumers were Spain (40%), Belgium (30%), the Netherlands and Greece.

In general, Russian exporters received an income of more than 15 billion dollars.

Pipeline gas

Despite the loss of Nord Streams, Gazprom continues to export gas to Europe (primarily to Austria, Hungary and Slovakia). Routes through Ukraine and Turkey operate for the organization of supply. Transit through the Ukrainian GTS amounted to approximately 15 billion cubic meters, and a total of over 15 billion cubic meters also passed through the Turkish “Blue Stream”.

Since the beginning of the full-scale invasion, China has become the main destination for Gazprom. By 2030, Russian companies plan to divert 85 billion cubic meters to the Chinese market. However, in order to implement the specified plans, it is necessary to build the pipeline “Power of Siberia – 2”, which is problematic. China is in no hurry to help Russia, realizing that Gazprom’s negotiating positions are quite weak. In addition, the price for contracts with China is lower than the average market prices. Thus, the reorientation to China will not allow to compensate the European market either in quantitative or qualitative indicators.

Almost 20 billion of gas went to Turkish consumers.

Despite everything, the total volume of exports of Russian pipeline gas amounted to 99.6 billion cubic meters. Taking into account price fluctuations, Russia’s final profit amounted to 35 billion dollars.

In general, all volumes of gas sales through pipelines and by sea reached 145 billion cubic meters, and the turnover amounted to at least 50 billion dollars.

To better understand the importance of oil and gas revenues, a simple analogy can be made: if military expenditures are planned at the level of 140 billion dollars in 2025, then Russian companies will receive a similar amount only from the sale of gas and the sale of oil on the Chinese and Indian markets.

Export structure of Russia

The ability of the Russian military machine to continue the war and balance the budget also depends on a positive balance in foreign trade. Details of indicators in the following tables.

|

Trade balance 2023 |

||||||||

|

Export |

Import |

|||||||

|

425 billion dollars |

285 billion dollars |

|||||||

|

Structure on the base of direction (in comparison with previous year) |

||||||||

|

Europe 84,9 billiard dollars ( – 68%) |

Asia 306,6 billiard dollars ( + 5,6%) |

Africa 21,2 billiard dollars ( + 43%) |

America 12,2 billion dollars ( – 40%) |

Europe 78,5 billion dollars ( – 12,3 %) |

Asia 187,5 billion dollars ( + 29,2%) |

Africa 3,4 billion dollars ( + 8,6) |

America 15 billion dollars ( – 11%) |

|

|

Structure (main positions) |

||||||||

|

Mineral products |

Agricultural production and equipment |

Export of services |

Main import is goods with highly additional value, technologies and machinery production |

|||||

|

260 billion dollars (60%) |

43 billion dollars (10%) |

99 billion dollars (23%) |

|

|||||

|

Positive balance |

||||||||

|

140 billion dollars |

||||||||

Thus, the export of mineral fertilizers (primarily oil, petroleum products, gas, etc.) provides more than half of Russia’s export revenues and creates a positive balance. Creating conditions for limiting revenues from the sale of oil and gas will significantly complicate Russia’s ability to support military expenditures.

The introduction of sanctions fundamentally changed the structure of Russian export revenues. It can be stated that the Russian side has lost almost 2/3 of the European markets. Gazprom ended the year with a deficit for the first time, and the Ministry of Finance has to save the company by reducing tax deductions.

It is an interesting fact that the significant quantitative growth of the export of products to the Asian direction is not accompanied by the expected increase in income. In monetary terms, the growth was only 5.6%. Such a trend proves that sanctions have a certain effect. Russian exporters are forced to give a significant discount on raw materials, which reduces trade gains.

Economic constraints have also minimized the prospects for the implementation of large-scale energy projects. For example, “Arctic LNG – 2” actually does not carry out commercial shipments, but the terms of putting Arc7 Arctic class gas carriers into operation. Periodically, there are difficulties with obtaining the appropriate equipment for the repair of oil refining complexes. However, these problems are of a strategic nature and are not critical to Russia’s ability to continue the war at this stage.

At the same time, Russian importers are finding workarounds for the import of dual purpose goods and important technologies – microchips, machine tools, etc. Such an adaptation allows Russian military-industrial complex companies to continue producing weapons for use in the war against Ukraine. In this context, sanctions have not yet achieved the desired result.

The complex situation with the Russian economy

The demonstrable growth of GDP provides arguments for Russian propaganda to talk about the development of the Russian economy. However, typical indicators of economic efficiency do not quite objectively demonstrate the situation in the specific Russian case. There are enough factors that indicate problems of a short-term and long-term nature.

Firstly, the positive GDP is due to the powerful stimulation of the state military-industrial complex. The Russian economy is focused on the production of military equipment and large-scale state investments in the sector. The rest of the economic sectors do not show such high results. The dependence of GDP on military expenditures through direct state intervention is increasing. In fact, the Russian budget receives income on foreign markets thanks to the oil and gas sector, after which the funds are sent to the military industry. There are no alternative mechanisms for ensuring the economy.

Secondly, Russia is experiencing a labor shortage. The unemployment rate has reached 2.4%, so demand in the labor market significantly exceeds supply. In conditions of unprecedented involvement of Russian citizens in the military-industrial production sector, as well as mobilization for war, other sectors of the economy are unable to meet their own personnel needs.

Thirdly, in order to stabilize the situation and in order to keep the economy within controlled limits, the Central Bank systematically increases the interest rate, and it has already reached the mark of 21%. All problems cannot be masked, and one of them continues to be high inflation – according to the results of 2023, it will be 7.42%.

Conclusions

1) Despite the demonstrable readiness of the Russian Federation to wage a war of attrition, the estimated safe margin for the Russian economy is 2 years without noticeable shocks.

With a high probability, already in 2026, the Russian economy will face the problem of replacing the budget deficit from the reserves of the National Development Fund and through deductions to the budget from oil and gas revenues.

The Russian leadership will have to choose between maintaining the planned expenditures for the war and further fiscal pressure on business and the population, forced refusal of strategic economic projects.

Economic problems will begin to manifest themselves more actively and will directly reflect on the Russian population in a negative way. The baseline scenario foresees the exhaustion of Russian monetary reserves already in 2026 and will prompt the Ministry of Finance to a new wave of tax increases;

2) Exhaustion of reserves will not lead to the complete inability of Russia to continue the war. However, the Government of the country and the power bloc will have to strengthen repressive measures in the economic sphere.

The complex of emergency response measures will include the nationalization of business assets, an increase in the tax burden, forcing citizens to transfer personal funds to the banking sector on a long-term basis without any guarantees of return (according to various estimates, up to 40 trillion rubles can be “in the hands” of businesses and the population – approximately more than 400 billions of dollars), compulsion to buy government bonds, etc.

Such a scenario will turn the Russian economy into a full-fledged military regime and lead to even greater repression by the regime against its own population, but it will make it possible to finance the war. However, in this format, the Government will not be able to distance the war from the population, the level of social discontent will grow, which will have to be restrained exclusively by forceful methods;

3) The Russian economy is “overheated”. There is no potential for real further growth in conditions of labor shortage and lack of technology. The Russian leadership has brought the situation to a dead end, when the situational growth of the economy depends exclusively on the state order in the defense sector, and the cessation of expenditures in the military industry will lead to a sharp decline in economic indicators. Russia is gradually approaching a severe recession;

4) The current economic situation – first of all, a significant shortage of labor force – does not contribute to a new official large-scale mobilization wave in Russia. Such a step will lead to further deterioration of the situation on the labor market and may become a significant stress for the Russian economy;

5) Due to the lack of external crediting opportunities and the ability to export products with high added value, oil and gas will remain the main part of external revenues. Their partial replacement is possible only by increasing the fiscal burden on other sectors. There are no visible prospects for the diversification of the economy. The overall situation will be favorable for Russia if discount Russian oil continues to trade at the level of 60+ dollars (for this, the US should not reduce the price cap, and the average price of Brent should not fall below 73 dollars per barrel);

6) Sanctions have a significant strategic destructive effect on the Russian economy, but do not cause critical damage to the Russian military machine. The situation may change drastically if the conditions are created for a further reduction in oil prices and secondary sanctions against companies from countries that help Russian importers circumvent sanctions.